Compliance operations

Pay Day Super From 1 July 2026: The 7-Day, 12% Compliance Workflow Every Childcare and Aged Care Provider Needs

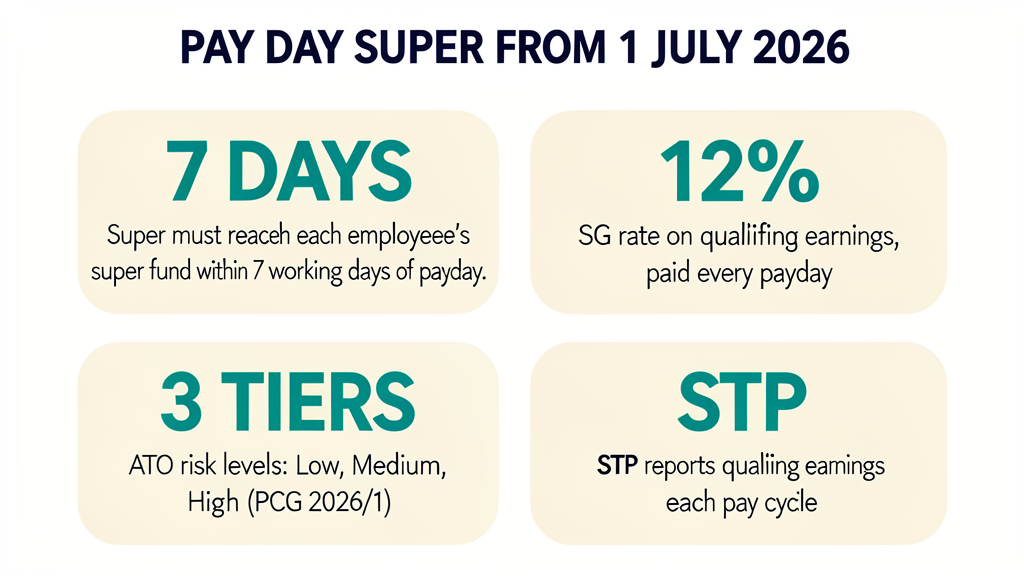

From 1 July 2026, every Australian childcare and aged care employer must pay super within 7 business days of every payday, calculate on qualifying earnings rather than ordinary time, and report both through Single Touch Payroll each cycle. The ATO has confirmed three risk zones for year one. Here is the compliance workflow that keeps your service in the Low zone.

From 1 July 2026, Pay Day Super is live across Australia. Every employer — including every Long Day Care, Out of School Hours Care, Family Day Care, In Home Care, residential aged care and home care provider — must now pay super guarantee on the same cycle as wages, with the contribution required to land in each employee's super fund within 7 business days of payday. The change moves the federal super guarantee payment from a once-per-quarter obligation with a 28-day grace window into a per-pay-cycle obligation measured in days, and the ATO has made clear that year one (1 July 2026 to 30 June 2027) is still a transition period — but only for employers who are genuinely trying to comply. Anyone who misses payments, pays late or pays to the wrong fund repeatedly will sit in Medium or High risk under PCG 2026/1 and become a live compliance target. This guide walks you through the four operational changes that matter for your service and the workflow that keeps your risk zone Low from day one.

What Pay Day Super actually changes on 1 July 2026

Pay Day Super replaces the quarterly super guarantee payment cycle with a per-pay-cycle obligation. The Australian Taxation Office (ATO) has published the change as part of its pre-1 July 2026 "About Payday Super" guidance (last updated 9 July 2026) and confirmed in a separate compliance bulletin — "Getting it right: compliance in the first year of Payday Super" (published 23 June 2026) — that year one is a transition year for employers who are genuinely trying to comply. The headline operational impacts for your service are four in number.

- The 7-business-day rule. Each super guarantee contribution must be received by the employee's chosen super fund within seven business days of payday. The day you pay qualifying earnings is day zero. The deadline does not pause for processing errors — if your clearing house takes longer than seven business days because of a data error, the contribution is still late.

- The base widened to "qualifying earnings". The 12% super guarantee rate is unchanged, but the base moved from "ordinary time earnings" to a broader "qualifying earnings" pool that includes ordinary time earnings, commissions, salary sacrifice contributions and other amounts previously counted as salary or wages for SG. For most childcare and aged care services this expands the base modestly — overtime is still excluded — but it widens the gap between an underpayment under the old rules and an underpayment under the new rules.

- Single Touch Payroll (STP) reports both qualifying earnings and super each pay cycle. Until 1 July 2026, STP could be reported with either qualifying earnings or super liability data; from 1 July 2026 the ATO expects both every cycle, with the year-to-date qualifying earnings label carrying the maximum contribution base for high-income earners who hit the cap. Payroll systems that capture overtime or allowances but do not push them into the qualifying-earnings bucket will create a reporting gap even if the cash flows correctly.

- Super funds have 3 business days, not 20, to allocate or return the contribution. The receiving end of Pay Day Super has been tightened to match the new employer deadline. Funds (and the SuperStream infrastructure) must allocate the contribution to the employee's member account — or return it for correction — within three business days. The combined effect is a system that runs on a roughly 10-business-day round trip per pay cycle from employer payment to member-visible balance, with every step in that round trip auditable.

The three ATO risk zones — and where your service lands

Practical Compliance Guideline 2026/1 (PCG 2026/1) is the document the ATO will use to triage every Pay Day Super shortfall in year one. The guideline defines three risk zones, and your zone is determined by your behaviour after a missed or late payment — not by whether you had a missed or late payment in the first place. If your super is paid in full, on time, to the right fund, you do not get a risk assessment at all.

- Low risk. You attempted to pay on time and for the correct amount, a contribution was not received (or was received without enough information to allocate), and you take steps to correct the issue as soon as reasonably practicable so that no unpaid super guarantee remains for that payday once resolved. The ATO will not focus compliance resources on Low risk employers even if they lodge a voluntary disclosure statement.

- Medium risk. You did not meet the Low-risk criteria but rectified any unpaid super guarantee within 28 days after the end of the quarter in which the qualifying earnings were paid. Compliance resources may be applied, but these cases are lower priority than High risk. Repeat patterns of quarterly cure push you towards High.

- High risk. You did not meet Low or Medium criteria — including situations where outstanding super guarantee amounts for one or more employees have not been corrected within 28 days after the end of the relevant quarter. Compliance resources are likely to be applied, and these cases are the highest priority. High risk attracts the full Super Guarantee Charge (SGC) plus Part 7 penalties and possible director-penalty exposure for related-entity employers.

The ATO has confirmed that employers can move between zones during year one depending on behaviour over time — paying late twice drops you from Low to Medium, fixing the issue promptly can lift you back. The risk assessment is a forward-looking operational score, not a one-off compliance stick.

What non-compliance now costs in dollar terms

Pay Day Super keeps the existing Super Guarantee Charge framework but applies it more often and on a wider base. The SGC comprises the unpaid super, notional interest (the ATO's compounding interest calculation on the unpaid amount), an administration fee, and an additional amount where the choice of fund rules have not been followed. The SGC and any associated penalties are not tax-deductible, which is the part most directors and finance committees misread — a missed pay cycle for 30 educators is not a deductible wage expense, it is an above-the-line compliance cost paid out of operating margin.

The typical exposure for a 50-employee long day care service with one missed fortnightly cycle works out to roughly $15,000 to $25,000 in unpaid super, plus notional interest, plus the administration fee, plus potential Part 7 penalties under the Superannuation Guarantee (Administration) Act if the ATO escalates from a notice of assessment to civil proceedings. For a 150-bed residential aged care home with one missed monthly cycle the numbers are an order of magnitude larger, because the wage base is larger and the contribution base is also wider under "qualifying earnings". This is why the ATO has said year one compliance focus is on employers not genuinely trying — the SGC economics alone are enough to make a one-off late payment a board-meeting agenda item.

- The late-payment penalty. If a contribution is received late by the employee's fund, the SGC is triggered. The SGC is non-deductible.

- The choice-of-fund penalty. An additional amount applies where you fail to comply with the choice of fund rules — including failing to offer a stapled fund when the employee does not nominate one.

- Part 7 penalties. These can apply on top of the SGC if the ATO escalates after a notice of assessment is unpaid, and can range from financial penalties to potential director-penalty exposure for some related-entity employers.

The compliance workflow that keeps you in the Low zone

The five-step workflow below is the same rhythm NovoCove uses with its childcare and aged care customers to keep Pay Day Super in step with the rest of the compliance calendar. None of the steps are hard by themselves; the discipline is doing every step on every cycle, every week.

- Step 1 — Lock the payroll calendar to a per-pay-cycle super run. Whatever your payroll cycle is (weekly, fortnightly or monthly), every cycle now has a super obligation attached. Bake the super payment job into the same runbook as the wage payment job — same day, same approver, same evidence pack.

- Step 2 — Re-baseline ordinary time earnings to qualifying earnings. Walk every award-covered role and every common allowance through the qualifying earnings checklist. For services with overtime, shift penalties or sleepover allowances, this is the place where most under-reporting historically happened — and where the new widest-base SG calculation will most often expose it. Update the payroll mapping, document the change, and re-test on the next pay cycle.

- Step 3 — Reconcile STP against the clearing house before submit. STP must now carry both qualifying earnings and the super liability each cycle, and the clearing house must report each contribution landed to the right fund. Reconcile them in the same workflow as your STP submit — a five-minute check that, if missed, becomes a 28-day cure window and a Medium risk classification.

- Step 4 — Track voluntary disclosure eligibility as an ongoing metric. The voluntary disclosure statement is now the ATO's recommended "show us you noticed" mechanism for one-off shortfalls that you cannot cure before the next quarter-end. Track which cycles need a VDS, lodge early, and record every notification timing in the same system that holds your STP evidence.

- Step 5 — Treat Pay Day Super evidence as part of your standard compliance pack. Year one is a transition year but the evidence pack you build now is the evidence the ATO will look at in year two if you drift into Medium or High risk. Hold per-cycle confirmation emails, clearing-house receipts, STP reports and (where applicable) VDS receipts in a single searchable archive that survives the personnel changes of the next two years.

How NovoCove handles Pay Day Super compliance

NovoCove's compliance workflow was built to hold employer obligations of this shape — recurring, per-cycle, with audit-ready evidence packs attached. The Pay Day Super changes fold into the platform as a configured Super Guarantee schedule that runs in parallel with your existing certification and qualification schedules. Each employee record carries the qualifying-earnings rate, the stapled-fund status, and the per-cycle super obligation; each pay cycle, the platform produces a Super Guarantee evidence pack with the STP report, the clearing-house confirmation, the allocation confirmation (where the fund publishes one), and the calculated risk-zone classification if a payment is missed.

For services that operate across multiple payroll cycles (common in aged care with weekly care staff and monthly salaried clinicians), NovoCove's per-cycle alerts catch the seven-business-day deadline on each run independently. For services with casual or rotating educators (common in OSHC and FDC), the platform's stapled-fund tracking keeps the choice-of-fund compliance audible at onboarding and surfaces the change whenever an employee fund moves. The same evidence pack that satisfies an ATO Pay Day Super review also satisfies a Department of Education or ACQSC audit on pay-and-conditions compliance — there is no second evidence trail to maintain.

For directors and owners, that means Pay Day Super slots into the NovoCove risk register alongside WWCC, NQF, SIRS and ACQSC audit cycles, with the same Friday-arising alerts, the same director dashboard, and the same Evidence Pack export that you already use for the regulator visits. You do not run a separate Pay Day Super software programme — you run NovoCove, and the regulator compliance is taken care of on every cycle.

This guide is general information and is not legal advice.