Aged care compliance

ACQSC Liquidity Standard Targeted Review: What Category 6 Residential Aged Care Providers Must Do Before July 17

From July 2026 the Commission is opening a targeted review of the Liquidity Standard that took effect when the Aged Care Act 2024 commenced on 1 November 2025. If you operate a residential aged care service in Category 6, you are in scope. Here is what the Commission will ask for, where the soft-touch educational intent meets hard section 142 penalty powers, and the 90-day workflow that keeps your licence and your registration on the right side of the regime.

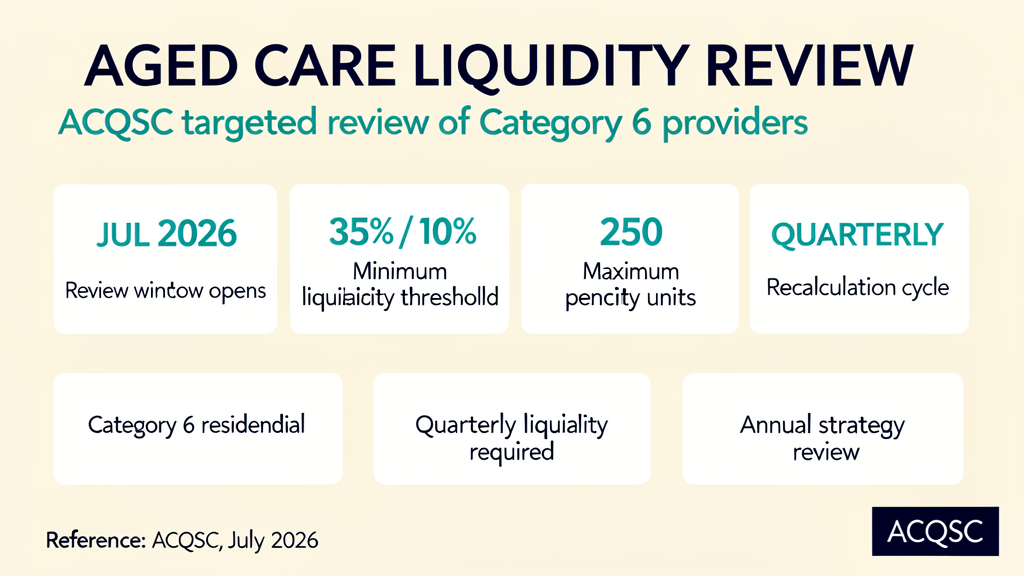

On 2 July 2026, the Aged Care Quality and Safety Commission announced in Aged Care Quality Bulletin #6-2026 that it would open a targeted review of the Financial and Prudential Liquidity Standard beginning in July 2026. Selected Category 6 residential aged care providers will be contacted this month. The Liquidity Standard is one of three new Financial and Prudential Standards that took effect when the Aged Care Act 2024 commenced on 1 November 2025, and compliance with it is a condition of registration under section 150 of the Act.

The Commission frames targeted reviews as primarily educational — a chance for the regulator to see how well providers understand the obligation and to support them to get it right, with escalation reserved for providers who disregard or fail to manage the risk. But the underlying obligation is non-negotiable. A provider that does not calculate and hold its elected minimum liquidity amount (MLA), does not maintain a written Liquidity Management Strategy (LMS), or does not keep a refundable deposit register where required, is committing a breach of a condition of registration. Under section 142 of the Aged Care Act 2024 the breach is a civil penalty provision carrying up to 250 penalty units, or up to 500 penalty units where the failure is significant or part of a systematic pattern of conduct.

This guide walks through what the targeted review is, what Category 6 providers need to have in place, the six board-level questions every responsible person should be able to answer with evidence today, and the 90-day workflow that turns the Liquidity Standard from a quarterly reporting chore into a live operational system.

What the targeted review actually is and is not

The ACQSC uses targeted reviews to focus on a specific obligation or a specific group of providers. The purpose is two-fold: it gives the Commission a structured way to test how well a cohort of providers understands a new obligation, and it gives the Commission an opportunity to work with providers who are not yet meeting the obligation before moving to formal enforcement. A provider who is genuinely engaging with the Liquidity Standard but is short of the threshold can expect remediation, not sanctions. A provider who is not engaging - who has not calculated the MLA, who has no LMS, who cannot produce evidence on request - should expect a different conversation.

According to the announcement in Bulletin #6-2026, the Commission may select a provider for the Liquidity Standard review if:

- the provider is at risk of not meeting its financial and prudential obligations

- the provider has not met its financial and prudential obligations in the past

- the provider is in a location, of a size, or of a type that the Commission wants to look at

- the Commission considers the review would benefit the provider.

If you are contacted, expect a structured request for documentation: the Quarterly Financial Report covering the most recent calculation period, the Liquidity Management Strategy as approved by the governing body, the calculation workpaper for your elected MLA, and where applicable, evidence that the refundable deposit register is being maintained. Selected providers will be contacted in July 2026 and the review window runs through to October 2026.

The 35% / 10% liquidity threshold: what it actually means

The Liquidity Standard does not impose a single one-size-fits-all cash buffer. Instead it requires each Category 6 provider to calculate both a default MLA and an evaluated MLA each quarter, choose which one to hold, and report on the choice. The default MLA is the figure that flows from the formula in the Standard - widely cited in sector briefings as 35% of cash expenses for all residential aged care providers, plus 10% of refundable deposit liabilities for providers that hold refundable deposits. Sector commentary from The Weekly Source records this as the "35 and 10 threshold" the Commission discussed in the original prudential-standards webinar.

If your organisation cannot meet the default MLA but can show that you have reliable access to alternate sources of liquidity (lines of credit, related-party loans, undrawn facilities) you can submit an Evaluated MLA notification form to demonstrate that you can still meet your obligations and cope with a financial shock. This is the second of two pathways, not a workaround. The Commission is explicit that the evaluated MLA must be supported by reliable evidence, that the notification form must be current, and that the LMS must reference both the default and evaluated figures.

What the threshold is really testing is whether a residential aged care provider can survive a financial shock without compromising care delivery and without leaving refundable deposit-holders exposed. The 35% of cash expenses buffer is calibrated to cover operating volatility (wages, utilities, supplier payment cycles). The 10% of refundable deposit liabilities buffer is calibrated to cover the next 12 months of accommodation-bond and refundable-deposit payouts. Together they are the floor that the Commission considers the minimum prudent holding for a well-run residential service.

What the Liquidity Standard requires you to have in writing

The Liquidity Standard requires three artefacts: a quarterly Liquidity Amount calculation, an LMS that the governing body has approved and that is reviewed at least annually, and a refundable deposit register where the provider holds refundable deposits, accommodation bonds or entry contributions. The artefacts are not optional, and the governing body approval is not optional. The Commission's Liquidity Standard guidance puts it directly: the LMS must include "a statement from the governing body that it is satisfied that the LMS meets the objectives of the Standard."

Beyond the three core artefacts, four supporting workpapers tend to be the difference between a smooth review and a difficult one:

- your Quarterly Financial Report for every period since the Liquidity Standard took effect on 1 November 2025, with the MLA election documented for each quarter

- a board minute or equivalent governing-body approval record naming the chosen MLA method and dated within the last 12 months

- the Annual Prudential Compliance Statement (APCS) for the 2025-26 financial year, completed in line with sections 166-380 and 166-385 of the Aged Care Rules 2025

- a register of related-party transactions and conflicts of interest for the governing body, so that liquidity movements involving related parties are transparently recorded.

Six board-level questions every responsible person must answer

Section 180 of the Aged Care Act 2024 imposes a due-diligence duty on responsible persons - meaning every board member, governing-body member, and senior officer who can influence the provider's conduct. The Commission expects responsible persons to maintain current, documented knowledge of the Financial and Prudential Standards and to be able to evidence that the provider has the resources and processes to comply. These six questions distil the Liquidity Standard into evidence prompts that board papers can be built around.

If your board cannot answer "yes — with documented evidence" to all six, it is carrying material compliance risk under the Aged Care Act 2024.

- Has the governing body formally approved a documented financial and prudential management system, and is that approval recorded in the minutes?

- Can you show that the provider's financial and prudential decisions support it remaining financially viable and sustainable, so it can continue to deliver safe, quality care?

- Is the APCS for the 2025-26 financial year audit-ready under Aged Care Rules 2025 (sections 166-380 and 166-385), with director-level visibility of conformance and at-risk items?

- Are responsible persons equipped to exercise due diligence under section 180, including current, documented knowledge of the three Financial and Prudential Standards?

- Are related-party transactions and conflicts of interest identified, registered and managed transparently, with a register that is current as at the last quarter end?

- Where the provider holds refundable deposits, accommodation bonds or entry contributions, are they safeguarded, properly accounted for, and recorded on the refundable deposit register required under section 150A?

The 90-day plan to pass the targeted review

The Commission has been explicit that targeted reviews are educational in their first phase, and providers who engage genuinely should not expect punitive action. The practical implication is that providers who use the window to bring their evidence base up to standard are rewarded, and providers who do not are flagged. The 90-day plan below turns the Liquidity Standard from a quarterly reporting obligation into a live workflow that any responsible person can review at any time.

Days 1 to 14 — establish the baseline. Pull together the existing LMS, the last four Quarterly Financial Reports, and the APCS working file. Map the documents against the six board questions above. Identify the questions where evidence is weak or missing. Document each gap and the owner assigned to close it. Present the gap register to the board at the next regular meeting and minute the owners and deadlines.

Days 15 to 45 — recalculate and refresh. Recalculate both the default and evaluated MLA for the most recent quarter using the Commission's liquidity calculator and the updated definitions of cash expenses and cash and cash equivalents that accompanied the Bulletin #6-2026 release. Confirm the elected MLA. Refresh the LMS to reflect the updated definitions and the elected method. Obtain governing-body approval at the next board meeting and minute the approval in the same vote as the LMS adoption.

Days 46 to 75 — operationalise the artefacts. Stand up the refundable deposit register if you hold deposits, and reconcile it to the most recent balance sheet. Implement a quarterly MLA calculation run that lives in a single system rather than across spreadsheets and emails. Stand up a director-visible dashboard that surfaces the elected MLA, the actual liquidity held, the gap, and the trend. Link the dashboard to the APCS so that director-level signoff is a single step at year end.

Days 76 to 90 — test and rehearse. Run a tabletop review with the same documents the Commission would request. Time how long it takes to produce each artefact from cold start. If any artefact takes longer than an hour to surface, fix it. Brief the responsible persons on the six board questions and rehearse the answers with citations. Update the APCS if anything material has changed during the 90 days.

How NovoCove handles this

NovoCove gives aged care providers a single system for the Financial and Prudential Standards, the APCS, the LMS, and the refundable deposit register. The platform auto-calculates the default MLA and the evaluated MLA each quarter using the definitions published by the Commission, flags any quarter where the elected MLA is at risk, and surfaces the calculation workpaper alongside the Quarterly Financial Report so that any responsible person can review and approve in a single click.

For the Liquidity Management Strategy itself, NovoCove templates the strategy against the Commission's guidance, controls the version, and captures governing-body approval with a timestamped minute. For the refundable deposit register, NovoCove links each deposit to the resident, the balance, the agreed payback terms, and the ageing of any outstanding amount - so that the register required under section 150A is always current and always production-ready.

For the targeted review workflow, NovoCove packages the artefacts the Commission will ask for - QFR workpapers, the LMS, the MLA calculations, the APCS, the refundable deposit register, the related-party register - into a single auditable evidence file that the responsible persons on the board can walk into a review meeting without rebuilding anything. Book a 20-minute demo and we will run a live liquidity-ratio drill against your last Quarterly Financial Report to show you what the targeted review window will ask of you and where your evidence base stands today.

This guide is general information and is not legal advice.